Ask five people in a contractor's office to explain the WIP schedule and you'll get five different levels of understanding — usually somewhere between “it's for the CPA” and “I know it matters but I couldn't defend it to a bonding company.” That gap is expensive. The WIP schedule is the single earliest warning system a contractor has for job profitability, and most of the value in it gets missed because people read the bottom line instead of the mechanics.

Here's a framework for reading it properly, with a worked example.

The Mechanics, In Order

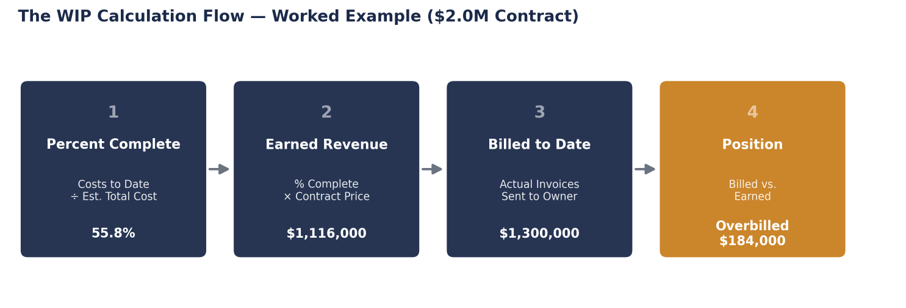

● Percent complete = costs incurred to date ÷ total estimated costs (cost-to-cost method, the industry standard).

● Earned revenue = percent complete × total contract price.

● Billed to date = whatever's actually been invoiced to the owner, independent of the above.

● The variance between earned revenue and billed-to-date is what lands on the balance sheet as either “costs and earnings in excess of billings” (underbilled) or “billings in excess of costs and earnings” (overbilled).

Every WIP line is really just these four steps for a single job. The schedule is the aggregation across your whole backlog.

Figure 1: The four-step WIP calculation, applied to the worked example below.

A Worked Example

Take a $2,000,000 contract:

|

Item

|

Amount

|

|

Contract price

|

$2,000,000

|

|

Original estimated cost

|

$1,600,000

|

|

Original estimated margin

|

20%

|

|

Costs incurred to date

|

$960,000

|

|

Revised estimated cost to complete

|

$1,720,000

|

|

Billed to date

|

$1,300,000

|

Percent complete = $960,000 ÷ $1,720,000 = 55.8%

Earned revenue = 55.8% × $2,000,000 = $1,116,000

Billed to date = $1,300,000, which exceeds earned revenue by $184,000 — this job is overbilled by $184,000

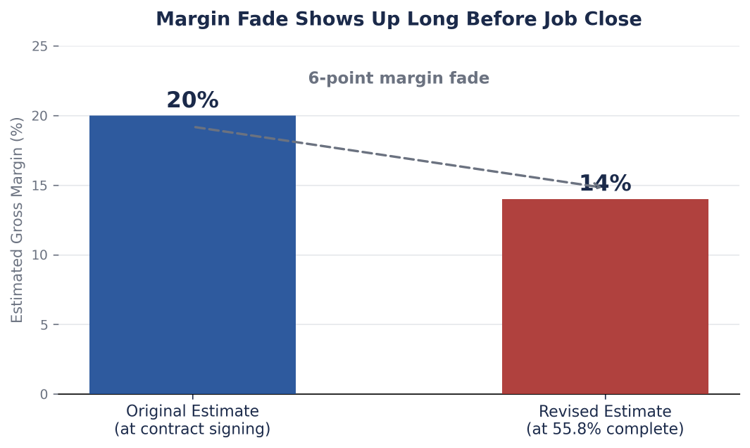

Now look at margin. Original estimated margin was 20%. Revised estimated margin is ($2,000,000 − $1,720,000) ÷ $2,000,000 = 14%. That's a 6-point margin fade — the job hasn't “lost money” on paper yet, but it's already told you where it's headed. Most offices won't catch this until closeout. A controller reading the WIP monthly catches it at 55% complete, while there's still time for the PM to act on it.

Figure 2: Margin fade from the worked example — a 6-point drop, visible well before job close.

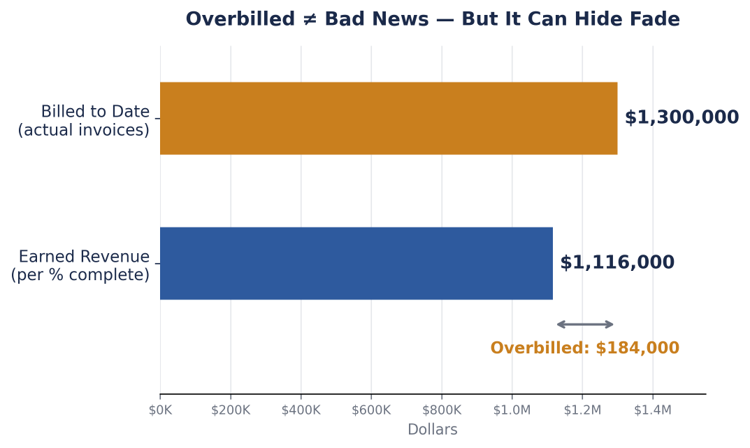

Why Overbilled Isn't Automatically “Good News”

An overbilled position feels like a cash cushion — you've collected more than you've earned. But combine it with margin fade, as above, and you get the classic construction failure pattern: the job looks fine because cash is ahead of earned revenue, right up until the float runs out near completion and the true, lower margin finally shows up as a loss. Overbilling doesn't cause the problem, but it can hide it for months. The question to ask isn't “are we overbilled?” — it's “is the overbilling shrinking, growing, or holding steady as percent complete increases?”

Figure 3: Earned revenue vs. billed-to-date for the worked example — an overbilled position of $184,000.

Underbilled Is Its Own Signal — And It's Not Always Bad Either

Underbilling often just means slow invoicing cycles or change orders stuck in approval — a process problem, not a profitability problem. But chronic, growing underbilling across many jobs is a cash-flow problem regardless of cause: you're financing the owner's project with your own working capital. If underbilled positions are large and growing across the backlog, that's a treasury conversation, not just an accounting note.

The Three-Line Check I'd Run Every Month

For every active job, track these three numbers side by side, month over month:

|

Check

|

What to ask

|

|

1. Percent complete

|

Is it moving at a believable pace given the schedule?

|

|

2. Estimated margin

|

Original vs. current — is it fading, and how fast?

|

|

3. Billing position

|

Over/underbilled — and is the trend growing or shrinking?

|

A job can look fine on any single one of these and still be in trouble. It's the combination and the trend that tell the real story.

Where This Connects to Bonding and Banking

Sureties and bank underwriters read WIP schedules exactly this way — they're not looking at your bottom line, they're looking for margin fade across the backlog and for balance-sheet reconciliation (WIP should tie precisely to the “costs/earnings in excess of billings” lines). A WIP schedule with unexplained margin fade across several jobs, or one that doesn't reconcile to the balance sheet, is one of the fastest ways to get a hard question from a bond producer — and one of the fastest ways to not get a question if it's clean.

The Takeaway

The WIP schedule isn't a compliance artifact for year-end. Read as a trend line — percent complete, margin, and billing position, together, month over month — it's the earliest place job profitability shows up, often months before it reaches the income statement. The contractors who avoid year-end surprises are the ones reading it that way all year, not just at close.